ASEAN’s trade exposure to GCC

The futurist Peter Schwartz wrote about a scenario in his book Inevitable Surprises where the US would become a “an isolated hegemon” or a “rogue superpower”. If one looks up the definition of international terrorism in 18 U.S. Code § 2331, one could reasonably conclude that the actions of both the Rouge Emperor and his devious apprentice meet the definition. Yet maybe this should not come as a surprise as every American President since Regan has (mostly illegally) bombed at least one Muslim country, usually in West Asia (Middle-East). Perhaps this is just a rite of passage. But I digress.

If playing chicken with the world economy is not enough for the Rouge Nation, ASEAN should brace for more trade turmoil: Rogue Nation III: Section 301 tariffs and Rogue Nation IV: Forcing countries to buy the ‘full stack’ of AI solutions from US consortiums or bundling AI hardware with data pipes and applications.

In this, and the next few posts, I will attempt to make sense of the exposure of ASEAN countries to this (avoidable) supply side shock and I am certain that anything I find will underestimate the eventual economic impact. The effects are showing up in many sectors, including domestic & international transport, hospitality & tourism, plastics & packaging, fisheries, and agriculture. In Singapore electricity generation uses natural gas and/or diesel so electricity prices have already gone up. Indonesia and Malaysia have decided to keep most of their fuel subsidies for now, but if prices are not allowed to adjust, they may have to eventually ration quantities. Since both the duration and outcome of the war are unknown, they may find that continuing these policies will seriously affect their fiscal position. Indonesia’s school meals program has already been criticized as being too ‘expensive’ from a budgetary standpoint; those costs are likely to rise as well. Thailand depends heavily on tourism; discounted hotel stays will have little impact if international aviation prices remain high. The spike in fertilizer prices will affect both costs and output so food security should be on the agenda as this is supposed to be an El Niño year.

As with any exogenous negative shock, the most vulnerable people, businesses and industries are hit first. In India for example one of the first clusters to be hit was ceramics and tiles in the western state of Gujarat, followed by the glass cluster in the eastern state of Uttar Pradesh. Both use propane and/or natural gas. India has no ‘strategic reserves’ of natural gas. Migrant workers are returning home to their villages just as they did during the pandemic.

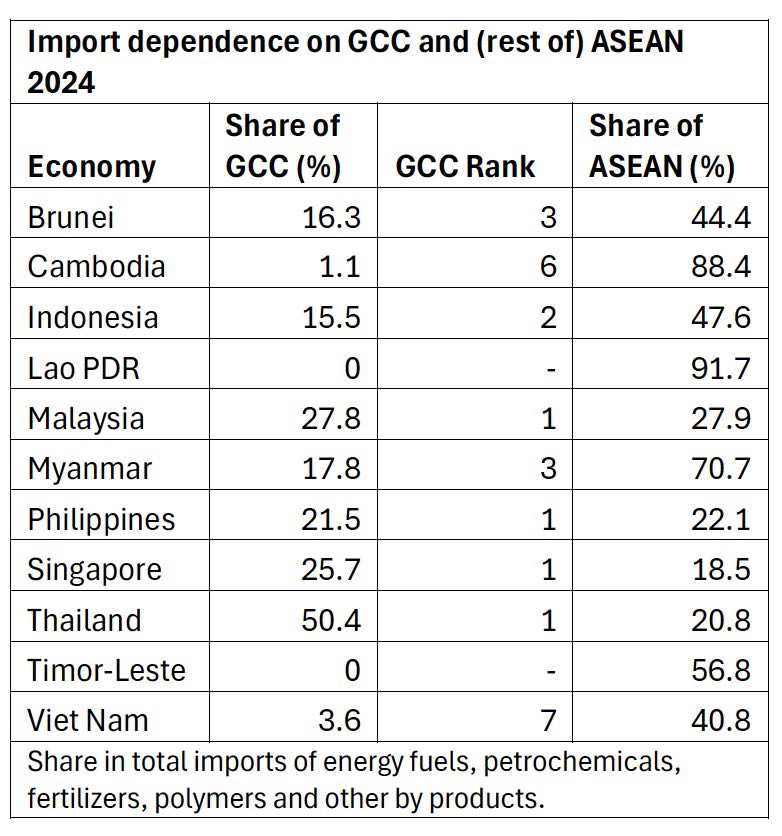

Here I provide trade exposure using a balanced trade database for 2024. I include imports of crude oil and gas as well as refined petroleum products and associated chemicals and by products (see notes).

The table below shows the import dependence of ASEAN economies on 10 GCC economies. It also shows intra-ASEAN imports. The top-10 import sources account for between 82 to 99% of imports of individual ASEAN economies. Three GCC countries are most important and frequently appear in the top-10 import sources of individual ASEAN economies: Saudi Arabia (8 times), United Arab Emirates (8 times) and Qatar (4 times). Oman is an important source for Cambodia and Myanmar.

From North-East Asia, China appears in the top-10 import sources for all eleven ASEAN economies, South Korea appears 8 times and Japan 3 times. Generally, smaller ASEAN economies such as Cambodia, Lao, Myanmar and Timor Leste rely primarily on ASEAN and/or ASEAN+3. The same is true for Viet Nam.

The large share of intra-ASEAN trade (or intra-ASEAN+3 trade) should not come as a surprise since many ASEAN countries have large refining and chemicals sectors including Singapore, Indonesia, Malaysia and Thailand. Vietnam is the newest entrant with two refineries (Dung Quat – domestic and Nghi Son – Japan/Kuwait JV) and Brunei has limited refining capacity. Singapore makes speciality chemicals; Thailand focuses on high volume commodity plastics resins etc. and Malaysia makes polymers and elastomers (elastic polymers). China is probably the largest refiner in the world (or at least in the same league as the Rogue Nation) and South Korea, which is another important import source for ASEAN is the fifth largest refiner in the world and a manufacturer of complex chemicals used in in the production of microchips and electrical batteries.

Once the dust settles, ASEAN should put the ASEAN electricity grid on the back-burner and every country should pursue the clean energy transition with a vengeance. The Thai auto cluster is already moving to producing electric cars and Indonesia has a battery industry in the making. In the long run it is better to sacrifice one or two industries than most of the economy. ASEAN should take full advantage of China’s so called ‘over capacity’ and ‘subsidies’. This will allow ASEAN to transform at low cost and at scale from the fuel of war and hegemony to the fuel of peace and self-reliance.

Notes

Four-digit HS (2022) categories included in imports table:

Energy fuels: 2709, 2710, 2711, 2714

Petrochemicals: 2901, 2902, 2905, 2909

Fertilizers: 3102, 3105

Polymers: 3901, 3902, 3907

By products: 2802, 2503

Sources

BACI balanced trade database (HS 2022)

Straits Times:

India’s ceramics and tiles industry faces shutdown as Middle East conflict disrupts fuel shipments, 6th March 2026.

Gulf war batters India’s glass heartland, testing New Delhi’s manufacturing drive, 2nd April 2026.

South China Morning Post:

Washington launches export initiative to ensure ‘future of AI is led by the United States’. 3rd April 2026.

Leave a comment